Introduction: From Bancor to Intercoin

At Bretton Woods in 1944, John Maynard Keynes proposed the Bancor — a supranational currency designed to settle trade balances between nations. It would have provided a neutral, algorithmic clearing mechanism. Instead, the U.S. dollar became the global reserve, and later the IMF introduced Special Drawing Rights (SDRs), a synthetic reserve asset tied to major fiat currencies.

But SDRs remain rationed by IMF allocations and serve governments, not people. Communities, cities, and smaller nations have little recourse when reserves dry up. Sri Lanka’s 2022 collapse, when the country literally ran out of foreign exchange and imports ground to a halt, showed how fragile the current system is.

The Intercoin system revives Keynes’ vision, but for the 21st century. It provides:

- A global settlement currency called INTER, functioning like a decentralized SDR, accessible to communities everywhere.

- A token for investors — the Intercoin InvesToR Token (ITR) — which funds development, rewards early team members, and provides aligned returns without destabilizing the monetary system. It might stop being a security once the system is deployed, thanks to no-action letters by the SEC to TurnKey Jet and Pocketful of Quarters

This separation of roles creates stability, compliance, and resilience.

INTER: the Internet of Coins

Intercoin X (INTER) is designed to be neither a security nor a commodity, but something else entirely. It is intended to become a secure, speculation-resistant settlement platform between communities:

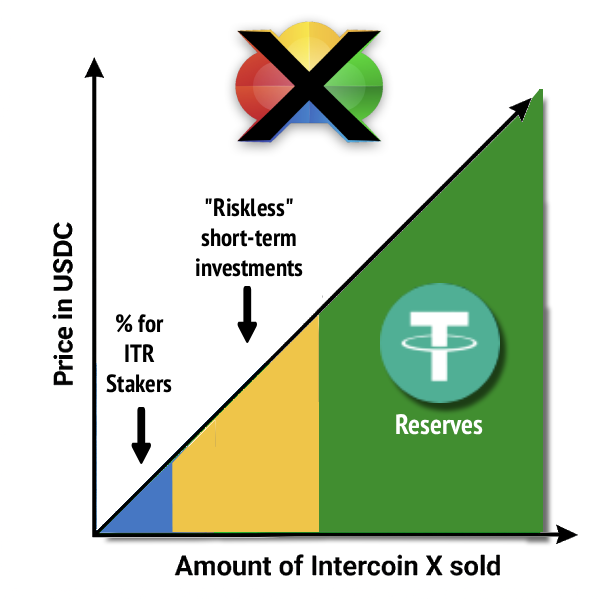

- Minted deterministically via bonding curves that accept ETH.

- Algorithmic pricing — everyone knows what INTER costs at every supply level.

- No insider allocations — INTER cannot be pre-mined, hoarded, or dumped.

- No derivatives or leverage — since communities, not speculators, are the only actors who interact with bonding curves, there is no overhang or futures market distortion.

INTER functions as a monetary system by the people, for the people. It is the settlement layer for community economies, much like SDRs are meant to be for nations — but without political rationing, IMF votes, or national hegemony.

Community Currencies and Sensitivity

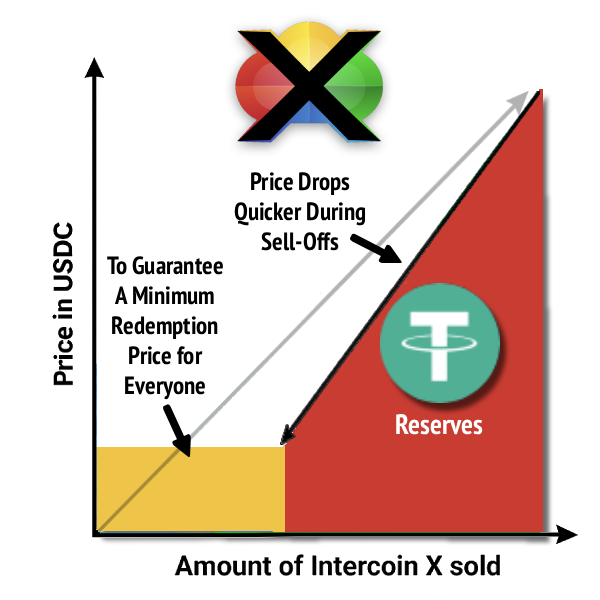

Communities issue their own coins backed by INTER reserves. Each coin’s redemption value is governed by three parameters:

- R = reserves held in INTER

- C = amount of circulating community coins

- s = sensitivity factor, between 0 and 1

The sensitivity factor is a smooth slider between two extremes:

- s = 0 → Hard peg: coins trade at par until reserves are gone (fractional reserve style).

- s = 1 → Floating share: each coin is a pro-rata claim on reserves (equity style).

- 0 < s < 1 → Blended model, enabling automatic stabilizers by communities.

This sensitivity mechanism allows communities to gradually devalue their coin during stress, rather than collapsing overnight. It replaces sudden bank runs with visible, smooth adjustments.

Historical analogy: In the 19th century, wildcat banks issued notes whose value depended on solvency, often failing suddenly. The Intercoin system encodes solvency risk in a transparent formula, turning hidden cliffs into gentle slopes. It can also enable stablecoins pegged to most mainstream outside currencies.

ITR: The Intercoin InvesToR Token

To raise capital for development and growth, the Intercoin system presold ITR (Intercoin InvesToR Tokens).

- ITR was sold to investors under SEC exemptions such as Reg D

- After holding for one year, investors are free to trade their ITR on secondary markets (see Rule 144 and over the counter (see section 4(a)(1) of the Securities Act of 1933)

- It continues to be allocated to investors, early team members, and strategic backers.

- Holders will be able to stake LP tokens of ITR Uniswap pools (e.g., ITR–USDT) to receive a share of the cash flows from INTER sales.

- When Intercoin’s platform launches, communities will buy INTER on its bonding curves (in exchange for USDC, USDT, ETH, etc.) and 3% of from all those INTER sales would go to the stakers, proportionally to their shares.

Why ITR Solves the Investor Problem

Bitcoin and Ethereum suffered from whale overhangs: early miners and VCs amassed huge token supplies, casting a permanent shadow over the market. Any time, these insiders could dump holdings, destabilizing the system.

The Intercoin system fixes this:

- Investors never hold INTER directly.

- Instead, they earn ETH dividends tied to ecosystem growth.

- Speculators are excluded — there is no way to hoard INTER supply or create derivatives on it.

This makes ITR a compliance-friendly security: clear roles, clear disclosures, aligned incentives. INTER remains a pure settlement currency, free from speculative distortion.

Analogy: ITR holders are stakeholders in the infrastructure of Intercoin, like owning stock in a toll-road operator. They earn a perpetual slice of traffic (ETH inflows) without hoarding the vehicles themselves (INTER).

Firewalls and Local Autonomy

The Intercoin system is designed to prevent contagion:

- Each community currency is siloed: if one treasury mismanages reserves, only its coin devalues. Other communities remain unaffected.

- INTER remains pristine: always backed by ETH via deterministic bonding curves.

- Investors are separated: they collect ETH royalties through ITR without holding INTER.

This firewall design solves problems that plagued past systems:

- The gold standard was stable but inflexible.

- The eurozone allowed fiscal contagion from Greece to threaten Germany.

- SDRs are political and rationed.

The Intercoin system avoids all three: stability, flexibility, and universal access.

Advantages of the Intercoin System

- Clear Roles: ITR = investor security, compliant and transparent… INTER = monetary settlement layer, not open to speculators. Communities = issuers of local coins, whitelisted by the Intercoin SRO to be able to hold INTER. Each one can have its own monetary and fiscal policy.

- Deterministic Supply: INTER minted only via bonding curves; no insider allocations.

- No Whale Overhang: Investors cannot hold INTER. No hidden supply waiting to dump.

- Automatic Stabilizers: Local coins devalue gradually, preventing sudden collapses.

- Local Autonomy: Communities set fiscal/monetary rules via sensitivity. No contagion.

- Investor Alignment: ITR holders earn ETH from adoption, not speculation.

- Compliance: ITR was initially sold as a security, making fundraising clear and lawful. INTER is designed to be neither a security nor commodity, obviating the need for regulation designed to rein in speculators.

Conclusion: A Monetary System by the People, For the People

The Intercoin system unbundles roles that traditional crypto and fiat systems conflated:

- INTER is designed to be an international settlement currency, like SDRs reimagined, but open to communities of all sizes around the world, rather than large countries and federations.

- ITR is an example of a secure, compliant way to raise capital and reward early backers, without contaminating the money supply.

The result is:

- A transparent, algorithmic, global settlement layer.

- Local currencies with sovereignty and built-in stabilizers.

- Investors aligned with growth, not speculation.

The Intercoin system is simply what money should be: by the people, for the people.