Given recent events, perhaps a good way to begin our look back at what Intercoin Inc. has accomplished is by putting it in a larger perspective of the technology sector as a whole. In the last few years, individual tech investors had a growing choice of vehicles, ranging from tech stocks to cryptocurrencies, ICOs to meme coins and NFTs. During frothy bull markets, various well-known companies adjacent to the crypto space offered sizable “yields” on money invested with them. But ultimately, how good were these investments for most people, and what did the projects accomplish?

As the Fed raised interest rates and speculative bubbles started bursting, a few key factors emerged as the main determinant of success: utility, mainstream adoption, and solid unit economics. Some teams built a useful product or platform, which went on to attract a global ecosystem of loyal users, who were willing to pay for use of the platform. Increasingly, these platforms have been open source and decentralized, owned by the community – examples include Bitcoin, Filecoin, Ethereum, and decentralized protocols built on top of them, like UniSwap and Aave.

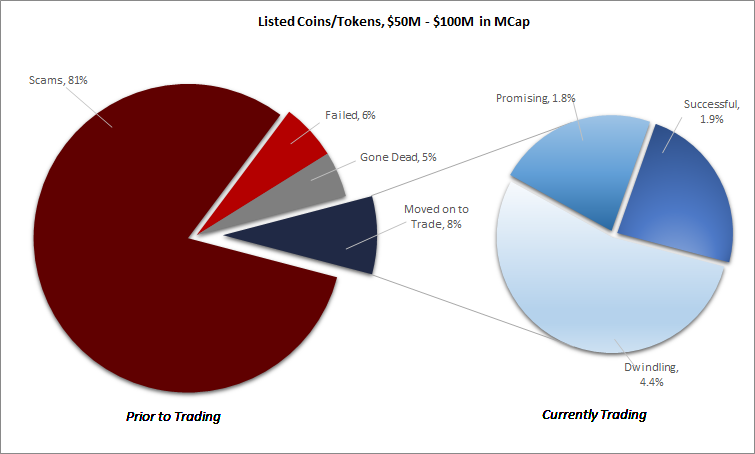

To the degree that projects departed from the above principles, they started to implode as speculators ran out of other people’s money. Back in 2017, a company named Block.One conducted the largest ICO in history, raising $4 Billion for EOS. With that kind of money, very little was actually built that fit the above principles, and now its own community considers it a failure. Meme coins like Shiba Inu, or ones with reassuring names like SafeMoon and EverRise did little but shuffle money around in a zero sum game, primarily redistributing money from later investors to earlier ones who cashed out. Poorly thought-through decentralized stablecoins like TerraLuna imploded losing over 99.9999% of their value in a week. A lot of this had to do with lack of useful products being developed and released that customers would be willing to actually pay for.

The centralized companies that were adjacent to crypto had some spectacular implosions too, but they were not even decentralized or open source. They were just a bunch of middlemen – the very thing that crypto was started to make unnecessary – who promised returns based on crypto bubbles. After Luna’s $40B market cap was wiped out, hedge fund Three Arrows Capital contributed to a $1 Trillion dollar crash in the crypto markets. They had previously bought the largest superyacht in Asia. Being over-leveraged by investing in guys like 3AC, trading platform Voyager and lending platform Celsius declared bankruptcy.

For a few months, the private founders of the two largest centralized exchanges, Binance and FTX, went around buying out distressed companies. But their feud ultimately led to a complete implosion of confidence in FTX, as a run on the exchange left the latter filing for bankruptcy. Other lending platforms, operated by companies like Nexo, Gemini and Gemini (owned by the Winklevoss Twins), had to suspend withdrawals from their yield-producing services, and as I write this, the latter two are facing the SEC for selling unregistered securities and failing to disclose risks, while Nexo is facing more serious allegations by authorities in London and Bulgaria.

It is tempting to look at the crypto market and conclude that blockchain technology isn’t good for anything but Ponzi schemes. But the vast majority of the failures have been due to speculators – hoping to make profits off some promised yield or ever-rising token prices – giving eye-watering amounts of money to a team of centralized middlemen, who proceeded to enrich themselves and invest the rest into the asset bubble, instead of building anything of use to a large number of customers. Centralized middlemen were precisely what decentralized protocols were designed to replace. Networks like Ethereum and Polygon led to an explosion of useful decentralized applications built on top of them, and people who kept their tokens in their wallet, secured with their own private keys remained fine. People who sent their tokens to centralized exchanges got “wrecked”, starting with MtGox in 2014, and until the present day. Blaming decentralized protocols for the corruption of centralized, crypto-adjacent middlemen, is like blaming gold and silver for the corruption of bank underwriters who issue loans.

But what about NFTs, memecoins and other seemingly worthless things? They are analogous to personal home pages on Web 1.0 when it first came out. Those who remember the original Web may recall lots of gaudy and tags, and sites on geocities that eventually all gave way to the modern Web. We went through stages, and search engines like AltaVista and Lycos gave way to Google, while Friendster and Myspace gave way to Facebook. Eventually, trillions of dollars were made on Web 2.0 business models like E-Commerce and Software-As-A-Service.

Some of this isn’t unique to Web 3. For years, the VC industry propped up businesses with utility and mainstream adoption but money-losing economics. Starting with Uber and Lyft, they dumped money-losing companies on the public in IPOs. Founders like Adam Neumann (WeWork) and Elizabeth Holmes (Theranos) were propped up by the VC industry for years, and had a net worth of billions, respectively. But importantly, these companies (except for Theranos) built useful stuff people were willing to pay for.

Companies such as Alphabet (Google), Meta (Facebook) and Twitter have historically made the vast majority of their revenues from advertising. Like crypto trading, though to a lesser extent, advertising is a zero-sum game between businesses offering goods and services, and has produced diminishing returns over the years (leading Google, YouTube etc. to compensate by showing ever more ads). As I write this, both Meta and Alphabet are down from their all-time highs, while Apple and Verizon are fine.